How to Keep Your Payment Processor From Freezing Your Dropshipping Account

A frozen payment account can stop a dropshipping business overnight. Learn why processors freeze accounts, the chargeback thresholds that trigger it, and how to stay safely below the line.

Ask any experienced dropshipper what keeps them up at night, and "a frozen payment account" comes up faster than almost anything else. A bad product launch you can recover from. A frozen processor account is different: your sales keep coming in, but the money stops flowing out to you sometimes for 90 to 180 days while your supplier bills, ad spend, and refunds keep marching on.

After more than 15 years helping merchants manage fraud and payment risk, I can tell you that account freezes are rarely random. They follow patterns processors watch for, and the single biggest trigger is one you can directly control: your dispute and chargeback ratio. This guide explains why dropshipping stores are flagged more often than most, the exact thresholds that put you in danger, and a practical plan to keep your account healthy and your funds flowing.

Why Processors Freeze Accounts in the First Place

A payment processor isn't being malicious when it freezes an account it's protecting itself from liability. Every time a customer files a chargeback, the processor is on the hook for the funds. If your store starts generating disputes faster than the processor is comfortable with, it limits its exposure: first with a reserve, then with a hold, and in the worst case, with termination.

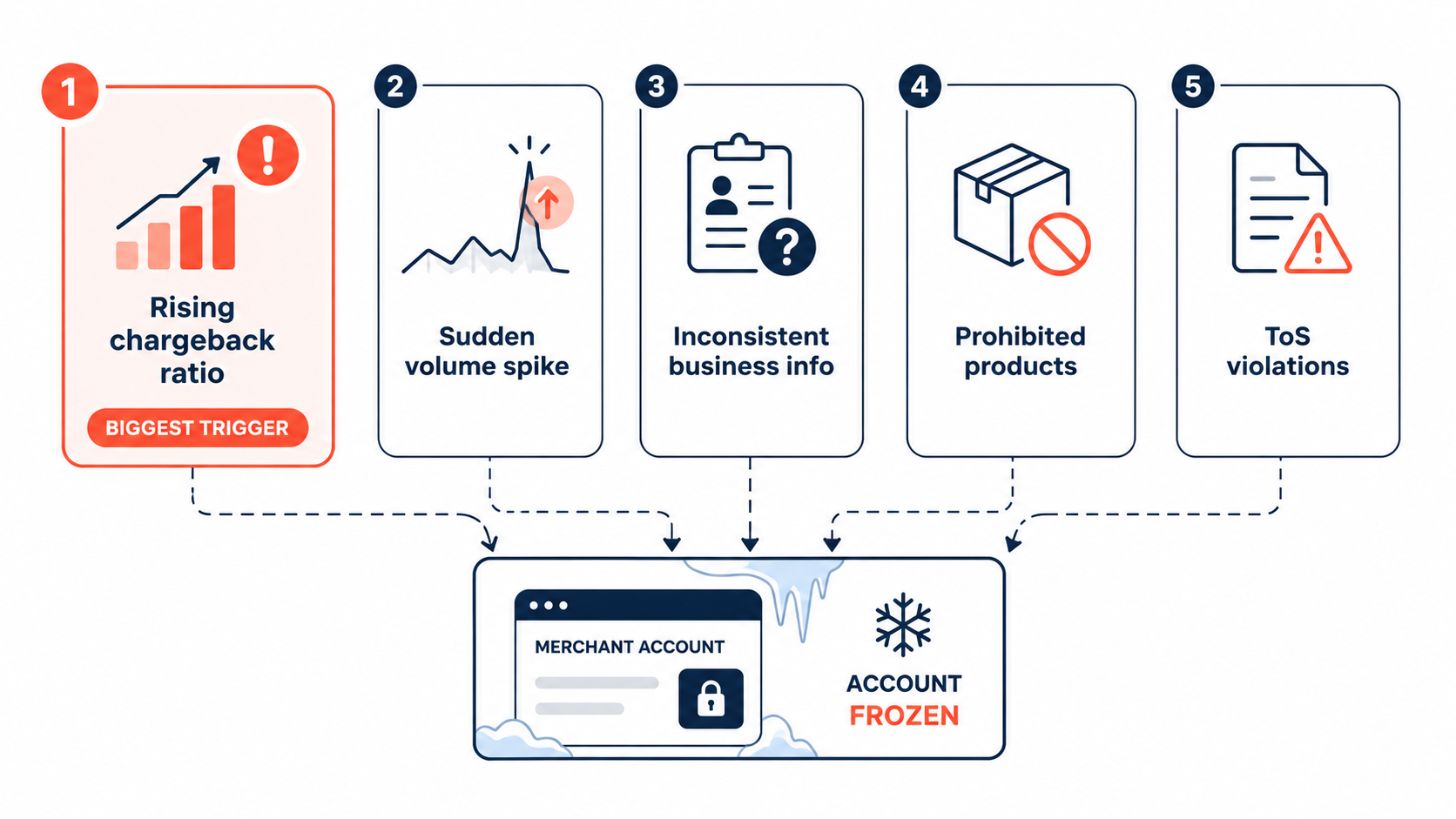

The most common triggers for a freeze are remarkably consistent across providers:

- A rising chargeback or dispute ratio by far the biggest one.

- A sudden spike in sales volume a viral product can look like fraud or money laundering to an automated risk system.

- Inconsistent or outdated business information mismatched details between your store, your processor, and your bank.

- Prohibited or high-risk product categories some processors restrict certain goods.

- Terms-of-service violations including patterns associated with deceptive marketing.

Aggregators like PayPal, Stripe, and Square are especially quick to act because they rely heavily on automated systems that can freeze an account without human review. Holds from these providers commonly last 90 to 180 days.

Why Dropshippers Get Flagged More Than Most

Dropshipping checks several of the boxes that risk systems are tuned to notice, which is why dropshippers face freezes more often than typical retailers:

Longer shipping times raise disputes. Third-party fulfillment and overseas suppliers mean longer delivery windows. The longer a customer waits, the more "item not received" disputes you collect and disputes are the metric processors track.

Volatile sales volume looks suspicious. Dropshipping is built on testing products and scaling winners fast with paid ads. A product that goes from 5 orders a day to 500 is great for business but reads as a red-flag anomaly to an automated underwriting model.

No inventory history means thin trust. A new store with no track record and a sudden burst of sales is exactly the profile processors reserve their strictest scrutiny for.

Friendly fraud inflates your numbers.

Because dropshipping creates expectation gaps, you accumulate more friendly-fraud disputes and as we'll see, the way disputes are now counted makes these especially costly. (For the full picture on why these hit dropshippers hardest, see Dropshipping Chargebacks: Why They Hurt More and How to Prevent Them and The Hidden Cost of Fraud for Low-Margin Dropshipping Stores.)

None of this means you're doing anything wrong. It means you're operating in a category that risk systems treat with caution, so you have to be more deliberate about staying inside the lines.

The Thresholds That Actually Trigger a Freeze

This is the part every dropshipper should commit to memory, because the rules tightened recently and many merchants are working from outdated numbers.

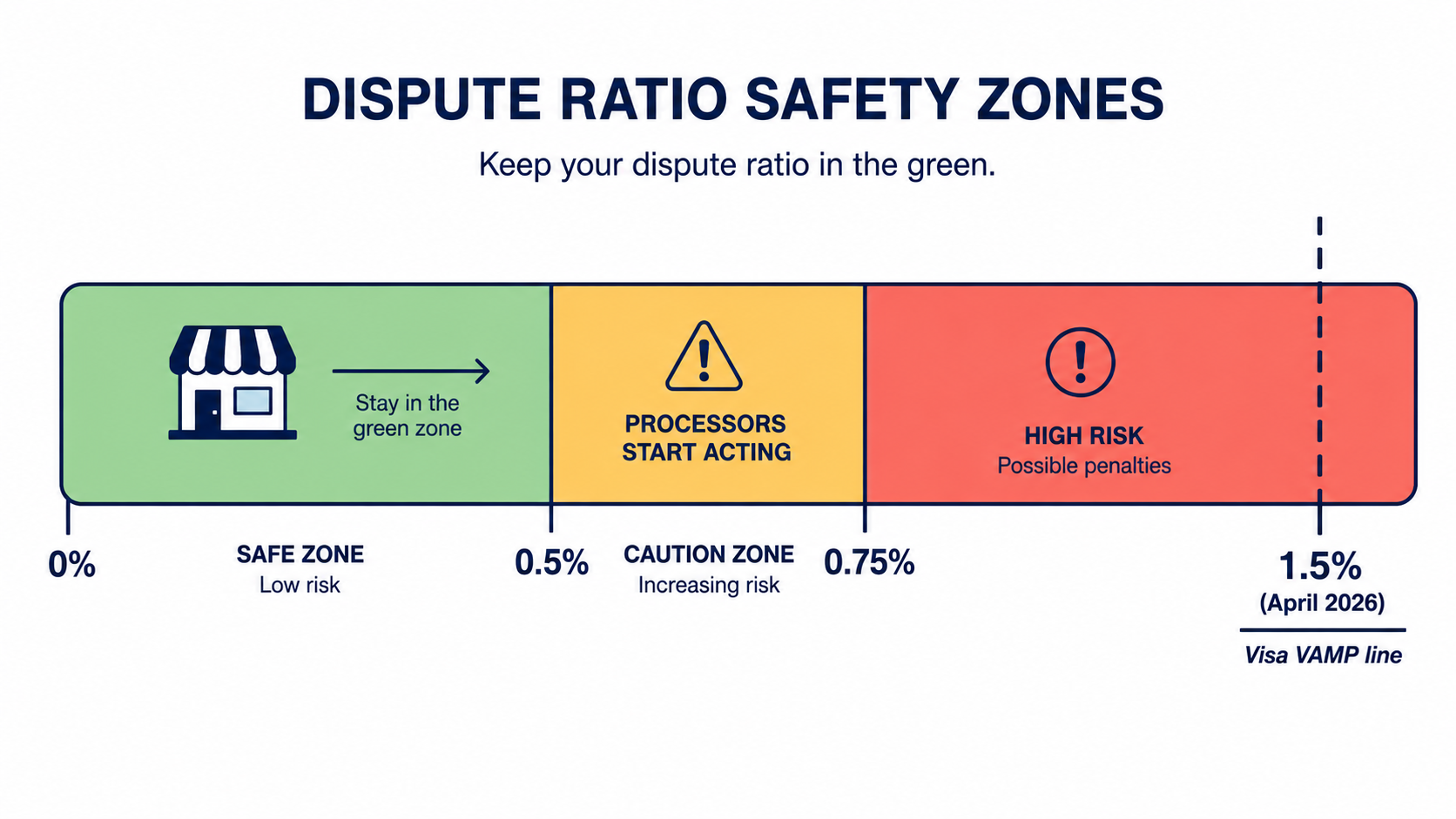

Visa's VAMP ratio

Visa's Acquirer Monitoring Program (VAMP) consolidated several older programs and set a merchant threshold of 2.2% when it launched in June 2025, then tightened it to 1.5% on April 1, 2026 for North America, the EU, and Asia-Pacific (some regions like CEMEA remain at 2.2%).

Here's the catch that trips people up: the VAMP ratio counts both fraud reports and disputes, not just chargebacks. That makes your VAMP number inherently higher and harder to manage than the simple chargeback ratio you might be tracking yourself. A store that thinks it's comfortably under 1% on chargebacks alone can be much closer to the VAMP line once fraud signals are folded in.

Mastercard's program counts differently

Mastercard's Excessive Chargeback Program (ECP) runs on different math it counts chargebacks only, not fraud reports. So you're effectively monitoring two separate compliance programs with two different calculation methods at the same time. Staying clean under one doesn't guarantee you're clean under the other.

Your processor's own comfort zone is lower

Card-network thresholds are the ceiling, not the safe zone. Your individual processor will often act well before you hit Visa's or Mastercard's official limit. In practice, many processors start imposing reserves, holds, or scrutiny once a merchant drifts toward the 0.5–0.75% range long before the formal program threshold. Treat anything approaching 1% as a warning, not a comfort cushion.

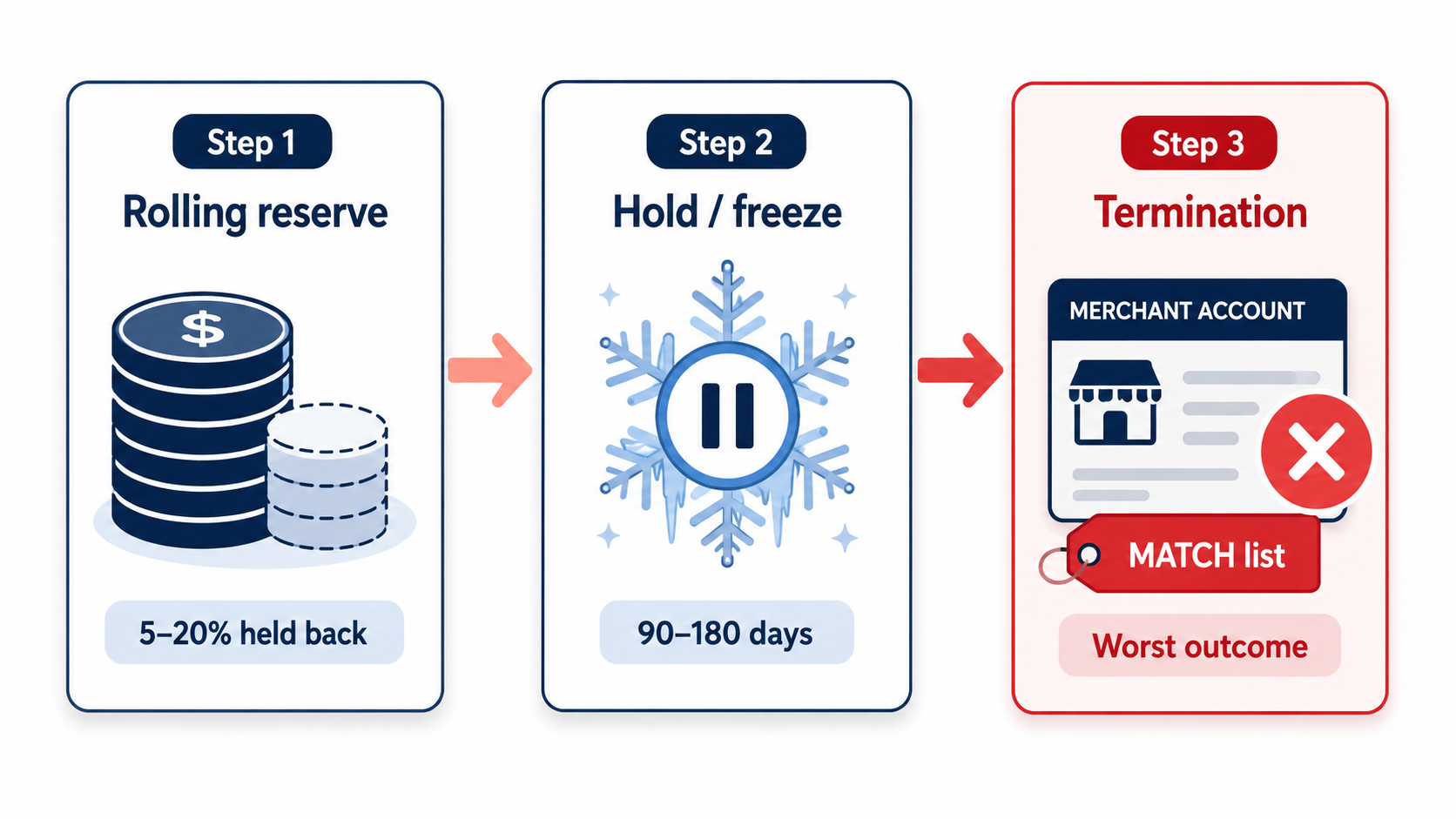

Reserves vs. Holds vs. Termination: Know the Difference

When a processor gets nervous, it usually escalates in stages. Knowing which stage you're in tells you how urgent the situation is.

Rolling reserve. The processor holds back a percentage of every transaction commonly 5% to 20% in escrow for 90 to 180 days, releasing it on a rolling schedule. Your business keeps running, but your working capital is throttled. A high chargeback ratio is often enough on its own to get a reserve imposed.

Temporary hold or freeze. Settlements stop while the processor investigates. This can last days, weeks, or the full 90–180 days depending on the provider. This is the stage that actually stops a dropshipping business, because you can't pay suppliers with money you can't access.

Termination. The account is closed and you may land on the MATCH list (a shared blacklist that makes opening a new merchant account much harder). This is the outcome you're trying to avoid at all costs, because it follows you to your next processor.

How to Keep Your Account Healthy: A Practical Plan

The good news is that the biggest trigger your dispute ratio is also the most controllable. Here's how to keep it well below the danger line.

Attack the three sources of disputes separately

Disputes come from three different places, and each needs its own fix:

- Fraud (stolen cards, bots) stop these before checkout so they never become orders.

- Shipping delays set honest delivery expectations and send proactive tracking updates.

- Product or expectation mismatch use accurate photos, clear descriptions, and a fair refund policy.

Lumping all disputes together and hoping a single tool fixes them is the most common mistake. The fraud slice and the friendly-fraud slice need different responses.

Stop fraudulent orders before they're placed

Since the VAMP ratio now counts fraud signals not just chargebacks keeping fraudulent traffic out of your checkout entirely protects your ratio in a way that fighting chargebacks after the fact never can. Screening for stolen-card patterns, card-testing bots, and anonymized sessions (proxy, VPN, TOR) before an order is placed keeps both your fraud reports and your eventual chargebacks down at the source.

This is where a dedicated fraud-prevention layer earns its place. An app like Browsify App scores visitor risk, detects proxy/VPN/TOR connections, fingerprints repeat offenders, and can automatically hold or block high-risk traffic before checkout with an iCloud Private Relay allowance so you don't accidentally block legitimate Apple users. It addresses the fraud slice of your disputes specifically; it won't fix a slow supplier or a misleading listing, so pair it with the fulfillment and communication fixes above. For a dropshipper trying to stay under a tightening VAMP line, reducing fraud disputes at the source is one of the most direct levers you have.

Smooth out volume spikes and keep records clean

When you're about to scale a winning product hard, a quick heads-up to your processor can prevent an automated freeze. Keep your business details consistent across your store, processor, and bank account. And document everything tracking numbers, supplier invoices, customer messages so that when disputes do come, you can fight the contestable ones and lower your net ratio.

Don't put all your eggs in one processor

If a single processor freeze can take your whole business offline, that's a structural risk. Many established dropshippers maintain a secondary payment option so a hold on one account doesn't stop sales entirely. It won't lower your dispute ratio, but it limits the blast radius if something goes wrong.

What to Do If Your Account Is Already Frozen

If you're reading this after a freeze, here's the calm version of the playbook:

- Read the notice carefully to identify the stated reason chargebacks, volume, information mismatch, or product category.

- Contact the processor's risk team directly and professionally; ask exactly what documentation they need.

- Submit evidence promptly fulfillment proof, supplier invoices, customer communications, and a clear explanation of any volume spike.

- Fix the underlying cause (usually the dispute ratio) so the same thing doesn't happen on your next account.

- Be patient but persistent holds often run their stated 90–180 days, but clean documentation and responsiveness can shorten the path.

Frequently Asked Questions

What chargeback ratio gets a dropshipping account frozen? Visa's VAMP merchant threshold is 1.5% (as of April 2026), and Mastercard's program uses separate math, but most processors act earlier often as you drift toward 0.5–0.75%. Treat anything approaching 1% as a serious warning.

How long do payment processor holds last? Commonly 90 to 180 days, especially with aggregators like PayPal, Stripe, and Square that use automated systems. Some investigative holds are shorter, lasting days or weeks.

Why is dropshipping considered higher risk? Longer shipping times generate more disputes, sales volume is volatile, new stores lack history, and friendly fraud is more common all signals that risk systems watch closely.

Does reducing fraud actually help my processor standing? Yes, and more than it used to. Because Visa's VAMP ratio now includes fraud reports alongside disputes, cutting fraudulent orders before checkout directly lowers the ratio processors evaluate you on.

Can I prevent a freeze entirely? You can't guarantee it, but keeping your dispute ratio low, your volume changes communicated, and your records clean dramatically reduces the odds. Prevention is far easier than recovery.

Final Thoughts

A frozen payment account is one of the few problems in dropshipping that can stop the whole business at once which is exactly why it deserves more attention than it usually gets. The mechanism isn't mysterious: processors watch your dispute ratio, the thresholds have tightened, and dropshipping's structure pushes you toward the line faster than most.

Stay on the safe side by attacking disputes at their three sources, stopping fraud before checkout so it never inflates your ratio, smoothing your volume changes, and keeping clean records. Do that consistently and the freeze you fear becomes a risk you've quietly engineered out of your business.

This article is for general educational purposes and reflects common e-commerce and payment-risk practices; it isn't legal or financial advice. Card-network thresholds and processor policies change over time and vary by region always confirm current Visa, Mastercard, and your processor's rules before making decisions.

Related Guides

- Chargeback Protection — Keep your dispute ratio low so processors never freeze your account.

- Stop Fake Orders on Shopify — The complete guide to identifying and blocking fraudulent orders.

- Card Testing Prevention — Stop carding attacks that inflate your fraud and dispute numbers.

- Automatic Fraud Blocking — Set up rules that protect your store 24/7 without manual review.